- Africa’s monetary unions bring stability, but weak public investment still limits economic development.

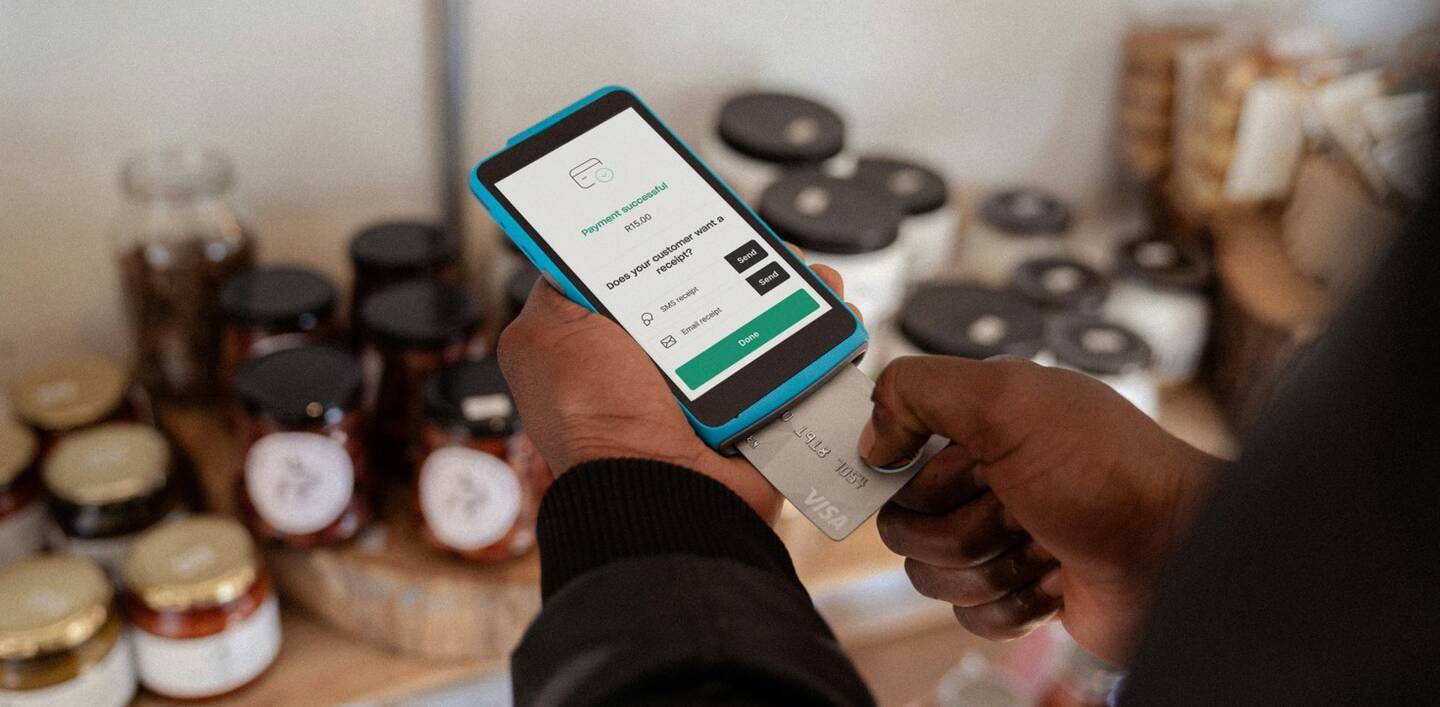

- Fintech is expanding financial access by bypassing traditional banking systems.

- Regulation and infrastructure gaps are slowing the scale-up of financial innovation.

The evolution of banking and financial technologies on the African continent is a geopolitical story. As governments, regulators, telecom operators, and international investors compete to shape financial infrastructures, control over payments, data, and credit flows has become a strategic lever of influence. Recent tensions between regulators and fintech firms in West Africa, alongside the growing role of global investors in funding African startups, illustrate how financial innovation is entangled with sovereignty, regional integration, and development priorities. Against this backdrop, the transformation of Africa’s banking sector reveals how institutional stability can both enable and constrain innovation.

Since their respective independences, many sub-Saharan countries have chosen to establish economic and monetary unions. Three are well known: the West African UEMOA (1994, 8 countries), the Central African CEMAC, and the Southern African CMA. In hindsight, these unions have contributed significantly to economic stability through a single currency, control of liquidity and monetary balances, and the management of inflationary risk.

Closing the Investment Gap in Public Goods

Such unions provide the expected economic and monetary stability. However, they are hampered by the weakness of member states’ investment policies, which affects, among other things, network and communication infrastructure, housing, and education.

The share of public investment also remains far too low, resulting in growing public deficits. As a remedy, public authorities could place greater emphasis on developing public-private partnerships. For instance, access to decent housing remains a challenge for families due to limited creditworthiness and restricted access to mortgage financing. Governments in many countries could also invest in education to address the considerable needs that require multi-year investment plans.

From Mobile Money to Fintech: Africa’s Banking Innovation

Africa is rich in banking initiatives. One of the most notable examples is the mobile money service launched in 2007 by M-Pesa in Kenya. This innovation is based on microfinance and money transfers via mobile phones.

Two aspects deserve further explanation. First, the telecommunications operator Vodafone acted as a new entrant to launch M-Pesa. Second, the adoption of these technological and social innovations has spread to about twenty countries, including some in Europe.

At present, innovation can also be found in the fintech sector. Competing with commercial banks, these companies offer mobile money and credit services and are better able to target merchants, artisans, and SMEs.

Fintech, Regulation and Inclusion in West Africa

Following a period of intense confrontation in West Africa, the banking regulator (BCEAO) and fintech companies have entered an era of dialogue. Faced with the BCEAO’s licensing requirements, fintechs are increasingly transforming themselves into banks or forming strategic alliances to survive and grow.

The BCEAO seeks to innovate in cross-border payment solutions, payment platforms, and cryptocurrency. Fintech companies combine mobile technology, artificial intelligence, and a deep understanding of local markets (youth, low-income populations, and rural areas).

They meet the needs of populations with limited access to banking services (less than 20%), who are young and digitally savvy. In this way, they contribute to a more inclusive financial system through greater transparency, simplicity, and speed.

Fintech companies offer technology-driven services such as digital payments, online banking, and international money transfers. This requires raising funds from investors in the African private sector. They face four main challenges:

a) insufficient national or regional infrastructure,

b) inadequate regulatory frameworks in certain regions,

c) difficulty in securing financing, and

d) low levels of financial literacy among the population.

The Future of the West African Banking System in the Face of Leapfrogging

This transformation, driven by fintech companies, represents a form of technological and financial leapfrogging. In many African countries, competition among commercial banks is intense, yet constrained by low levels of financial inclusion. Banks tend to target the same customers: large corporations and the public sector. Major pan-African financial groups are contributing to the consolidation of the industry.

Regulation remains a major obstacle for fintechs, as legal frameworks are often ill-suited to new financial models. Some African governments, fearing a loss of control over their financial systems, have imposed restrictions on fintechs.

Fintechs are still small in scale, both in terms of workforce and business activity. Access to financing remains another challenge. Although fundraising has increased (over $3 billion in 2023), investors are primarily international funds, while local investors remain more conservative, which affects the survival rate of fintechs.

Finally, technological infrastructure remains a barrier in certain regions. Since 2021, digital financial solutions have enabled millions of people to enter the formal economy. Technology and service innovation can help bridge gaps in traditional infrastructure and create new business models.

Sources

Article written by Professor Bertrand Quélin, based on his observations on the evolution of the African banking landscape.